Health insurance decisions often begin with clearing basic misconceptions and understanding the role insurance plays over the long-term. Having the right health insurance is not just a financial decision it is a form of long-term risk management as well.

In our previous blog, we had addressed these foundational aspects. Once those fundamentals are in place, the real challenge begins.

With multiple options in the current insurance landscape, choosing the right health insurance policy is no longer straightforward. This blog explores the key details on how to evaluate options carefully and offers a practical action checklist to help you build effective real-world coverage.

I. Assess Yourself before You Choose

Health insurance is not a one-size-fits-all product, and what works well for one person may be inadequate for another. Hence, it all starts with understanding your own risk profile. A clear self-assessment helps you decide how much coverage you need, which policy suits you best and where the risks lie:

- Work profile and lifestyle: Physically demanding or travel-intensive roles may require stronger accidental coverage, while sedentary or desk-based work increases exposure to lifestyle-related conditions, thereby requiring stronger coverage for critical illnesses.

- Your family composition: A family floater would be generally suitable for you, your spouse, and children, while elderly parents are better covered under separate policies. While separate policies do involve paying an additional premium, adding them to the same floater moves the policy into a higher age-based pricing band and raises the risk of the shared coverage being exhausted by more frequent claims.

- Existing health conditions and medical history: These impact waiting periods, exclusions, and future claim eligibility. Knowing this upfront helps to plan the coverages and avoid unrealistic expectations.

II. Choose the Right Insurer

Health insurance is ultimately a promise of support during medical emergencies, which makes choosing the right insurer just as critical as choosing the right policy.

- Claim Settlement Track Record: Not just the claim settlement ratios, one needs to look for consistency over years, patterns in claim rejections, and average claim disposal time. These details are available in the insurer’s annual reports, Insurance Regulatory and Development Authority of India (IRDAI) public disclosures, and independent industry comparisons, and they provide insights into how reliably claims are handled.

- Hospital Network Coverage: Review the insurer’s latest list of network hospitals on its official website and verify whether leading hospitals in your city and quality healthcare providers in nearby towns are included. A strong network means seamless access to cashless treatment and reduced last-minute complications.

- Claims Processing Experience: Go through policy documents and product brochures to assess documentation requirements, approval timelines, and cashless settlement conditions. In addition, customer reviews and claim experience feedback can help highlight how transparent and responsive the insurer is in real situations.

III. Strengthen the Policy with Essential Add-ons

A basic health insurance policy is rarely sufficient in today’s healthcare environment, and hence there would be gaps between what is covered and what is billed. Carefully chosen add-ons help to bridge these gaps and make your coverage more aligned with and at par with the real-world needs.

- Power booster: Automatically refills the sum insured if it gets exhausted and, in some policies, also provides additional coverage over the base sum insured. This helps to manage multiple hospitalisations and partially counter rising medical costs.

- Non-medical consumables: Hospital expenses such as gloves, masks, PPE kits, syringes, and other consumables are typically excluded from standard policies. This add-on ensures these costs are covered, preventing avoidable out-of-pocket expenses.

- Co-payment waiver: Many policies, especially those covering senior citizens, include a mandatory co-payment. This add-on removes or reduces the percentage of expenses you must pay from your own pocket during claims.

- Critical illness rider: Provides a lump-sum payout upon diagnosis of specified critical illnesses, offering financial support beyond hospitalisation costs for income loss, recovery, or lifestyle adjustments.

IV. Be Generous with Your Coverage: Take a Super Top-Up

The biggest risk in today’s insurance landscape is inadequate coverage. What seems sufficient today will only be a penny after a few years. This is why reaching the adequate coverage is essential, and super top up arrives as a saviour. Instead of increasing the base sum insured at a high premium, a super top-up offers a more efficient way to enhance your coverage.

For example, for a 30-year-old, a ₹10 lakh base health insurance policy may cost around ₹8,000–₹15,000 per year, while adding a ₹3 crore super top-up with a ₹10 lakh deductible can cost as little as ₹2,000–₹4,000 annually. This combination allows you to secure a high overall coverage at a fraction of the cost of increasing the base policy.

Top-up vs Super top-up

A regular top-up policy pays only when a single hospitalisation bill exceeds the deductible (a deductible is the amount of medical expense you must pay or your base policy must cover before a top-up or super top-up pitches in), whereas a super top-up considers the total hospitalisation bills in a policy year.

For example, if you have a ₹5 lakh deductible and incur two hospitalisations of ₹4 lakh each, a regular top-up will not pay anything, but a super top-up will cover ₹3 lakh once the total expenses cross ₹5 lakh. This makes super top-ups more prominent and practical for managing recurring medical treatments.

V. Disclose, Document & Review Regularly

Health insurance works effectively only when the information provided is accurate and the policy is kept relevant. Many claim rejections occur not because the coverage is inadequate, but due to non-disclosure or insufficient documents. Honest disclosure, clear documentation and regular reviews ensure your policy remains valid, relevant and claim-ready.

- Declare pre-existing conditions, past treatments, and lifestyle habits at the time of purchase and renewal to avoid claim disputes later.

- Keep medical reports, hospital bills and claim forms organised and accessible, as these are essential for smooth claim processing.

- Add new family members such as a spouse or newborn without delay to prevent gaps in coverage.

- Missing a renewal can reset waiting periods, remove accumulated benefits, and cancel valuable add-ons, disrupting your long-term protection. Never miss the timelines!

- Assess regularly if your coverage is still sufficient, add-ons remain relevant, and whether your overall protection needs to be enhanced in line with changing life stages.

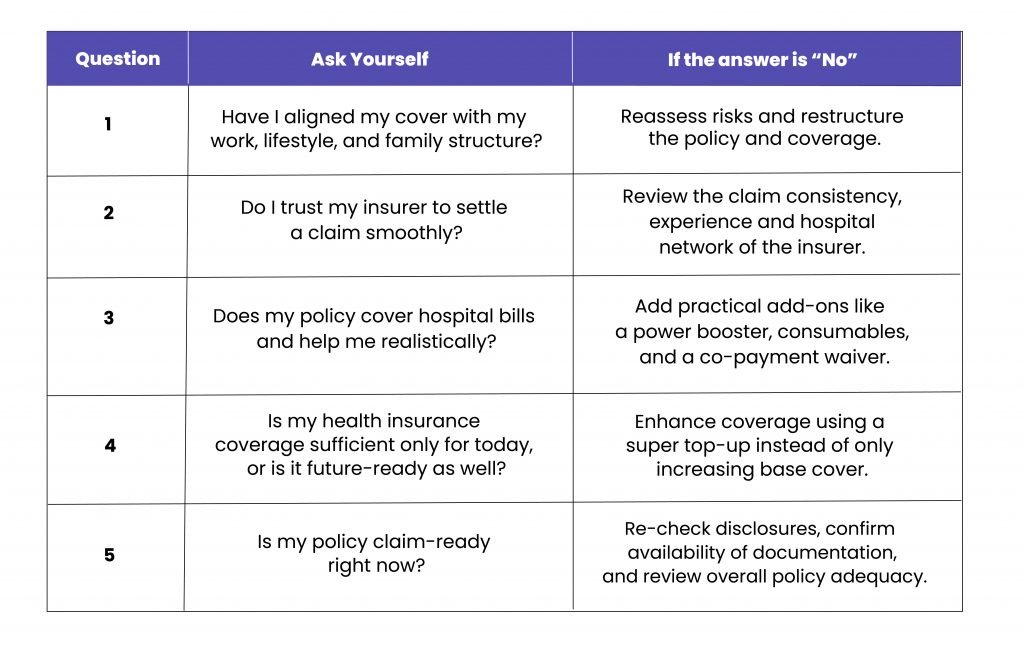

VI. A Quick Reality Check for Your Health Insurance

Conclusion

Health insurance delivers value only when it can work seamlessly during a medical emergency. The difference between a stressful experience and a smooth one often lies in how thoughtfully the policy has been structured and kept relevant over time.

By taking a deliberate approach today, you not only protect yourself from immediate medical expenses but also build resilience against rising healthcare costs, financial planning disruptions, and changing life needs. In the long run, the right health insurance strategy, along with sound financial planning, is also about peace of mind.

Contributors:

N Srilatha Bhat – Linkedin

Kuldeep Sarma – Linkedin

Poonam Vernekar – Linkedin

Leave a Reply