Life is full of surprises. Some are pleasant ones, while some may not be so. While emotions take centre stage during major life events such as marriage, parenthood or buying a home, these events bring in certain financial implications. If not planned for properly, they can lead to consequences such as falling into unmanageable debt or falling behind on long-term goals. Therefore, financial preparedness is crucial for securing your future. This article explores how to plan for major life events while ensuring long-term stability for you and your loved ones.

I. The Foundation Before All the Big Events

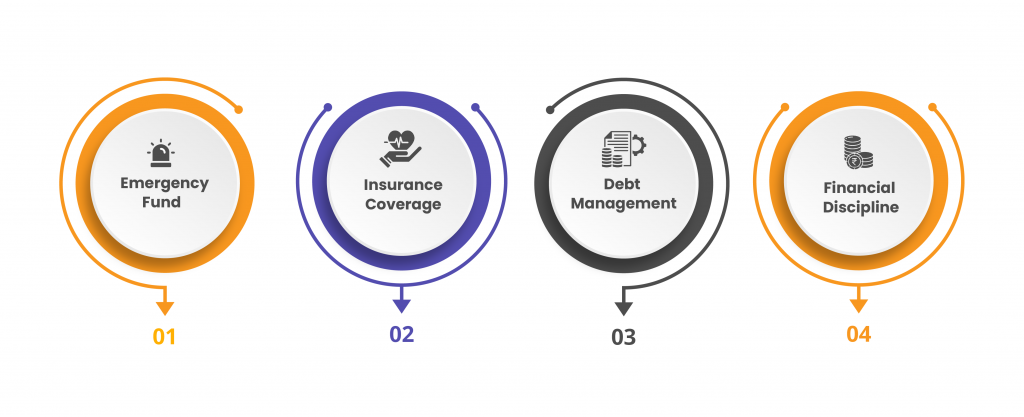

A. Emergency Fund: Create an emergency fund that covers at least 6-12 months of your monthly essential expenses to safeguard you from any unexpected situation. For detailed tips on building an effective emergency fund, check out our previous blog here.

B. Health and Life Insurance Coverage: Ensure you have adequate health and life insurance coverage to protect yourself and your dependents, and to avoid unforeseen financial burdens during medical emergencies.

C. Debt Management: Pay off high-interest debts and avoid unnecessary new credit. At the same time, loans such as home or education loans can be “good debt” if managed well. Good debts allow you to preserve cash for investments that can generate higher returns than the loan interests. Managing debt responsibly improves your credit score, reduces financial stress, and enables you to save for future goals.

D. Financial Discipline: Financial discipline is critical for the financial foundation you need before planning major life events. Setting clear financial goals and tracking your spending with a realistic budget ensures you stay on track. This enables you to navigate life’s bigger events smoothly and securely.

II. Tie the Knot Without Financial Knots

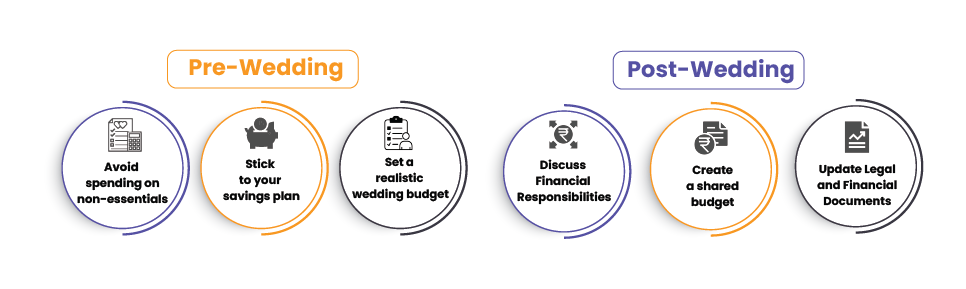

A. Pre-Wedding Financial Planning

2. Stick to your savings plan: Do not ever compromise your emergency fund or long-term savings for one day of celebration.

3. Set a realistic wedding budget: Plan in advance and start saving for your dream day, while ensuring you do not dip into savings meant for long-term goals or emergency funds. This allows you to enjoy the celebration without compromising your financial security.

B. Post-Wedding Financial Planning

2. Create a shared budget: Align your budget with monthly expenses, savings, and major plans such as buying a home or travel. Decide how each partner contributes and manages expenses within this budget to ensure both are on the same page financially.

3. Update Legal and Financial Documents: Update the necessary changes, such as changing of nominees for your accounts, insurance beneficiaries, and emergency contacts to reflect your new marital status.

III. Parenthood: Planning Beyond Diapers

Welcoming a child is a joyous moment, but parenthood comes with many expenses even before the baby arrives. From diapers to daycare and beyond, costs can add up quickly. Therefore, your budgeting for parenthood should consider a systematic approach:

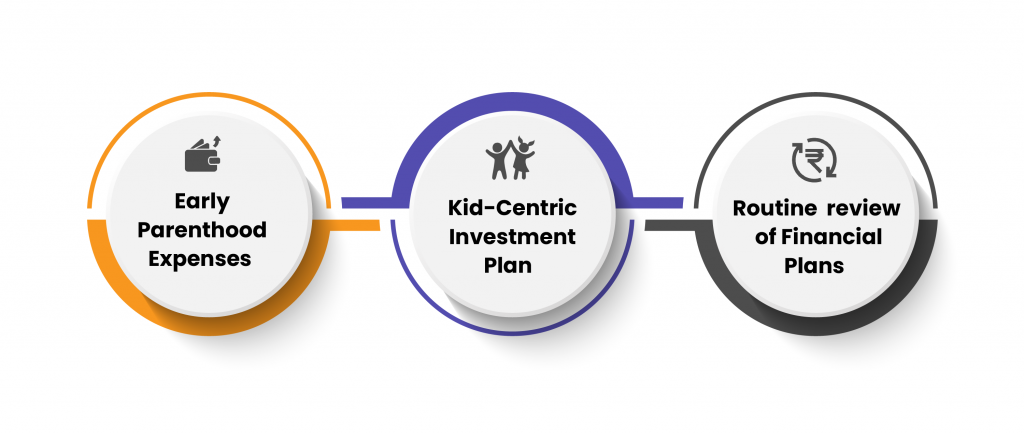

A. Early Parenthood Expenses

Initial expenses like hospital delivery (approximately ₹70,000 – ₹2 lakhs in private hospitals in India), baby gear, childcare must be assessed and budgeted for in advance. Review health insurance coverage and be prepared to revisit your budget if income changes after childbirth, such as when one parent takes a break from work.

B. Kid-Centric Investment Plan

Start investing in SIPs (Systematic Investment Plans), child-specific mutual funds and government schemes as early as possible to build a strong financial base for your kid’s education and future. You can also read our detailed blog on SIPs here to understand how starting early can work in your favor.

C. Routine review of Financial Plans

Parenthood brings new responsibilities and expenses, so it’s important to monitor your financial plans to safeguard your family. Regularly review insurance coverage and investments, and adjust annually based on changing needs, rising costs, or new family responsibilities.

IV. Buying a Home: Financial Checklist

For Indian households, buying a home is not just buying a place to live in. It is a major investment for the safety, security and happiness of their loved ones. Here’s a checklist of key things to consider before investing in your dream home:

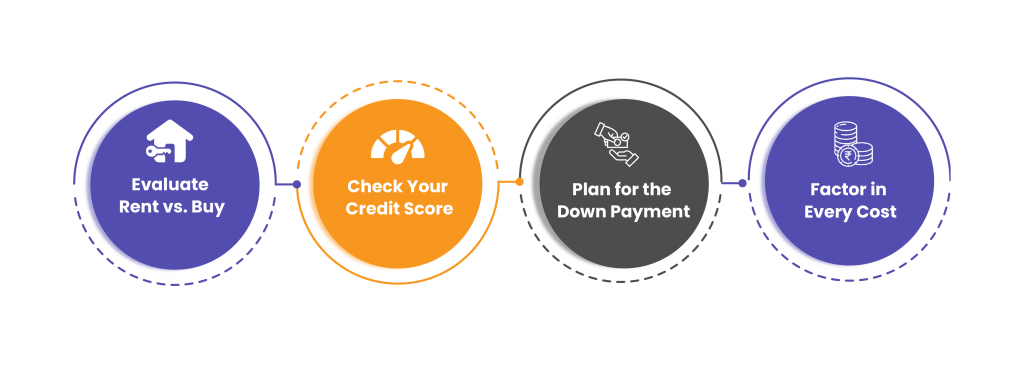

A. Evaluate Rent vs. Buy: Carefully analyse whether it is renting or buying that suits your current financial situation and long-term goals. For a detailed comparison and insights, check out our previous blog here.

B. Check Your Credit Score: Credit score is crucial, as it impacts loan approvals and interest rates. A higher score can help you secure better terms.

C. Plan for the Down Payment: Plan your down payment based on what you can comfortably afford without straining your finances. In some cases, taking a home loan while investing your available cash elsewhere may offer better financial benefits. So, consider your overall investment strategy before deciding on the down payment amount.

D. Factor in Every Cost: Estimate all costs carefully, including stamp duty, registration fees, property taxes, and monthly EMIs. Set aside a post-purchase buffer for interiors, maintenance, and unexpected repairs to avoid financial surprises after moving in.

V. Conclusion

Life is unpredictable, but smart financial planning can make major milestones more manageable. The steps may seem small and simple, but they require financial discipline and conscious effort to implement. At Advith ITeC, our PFM (Personal Finance Management) team helps you plan and manage your finances enabling you to achieve your goals with confidence. Start early, stay disciplined, and let your finances work for you.

Contributors:

N Srilatha Bhat – Linkedin

Kuldeep Sarma – Linkedin

Poonam Vernekar – Linkedin

Leave a Reply